People spending less to so they can pay mortgage

Australian borrowers in Western Sydney have “rallied around the home” and focused on paying their mortgage during times of rate rises and financial stress, according to West Side Capital managing director Tony Nguyen.

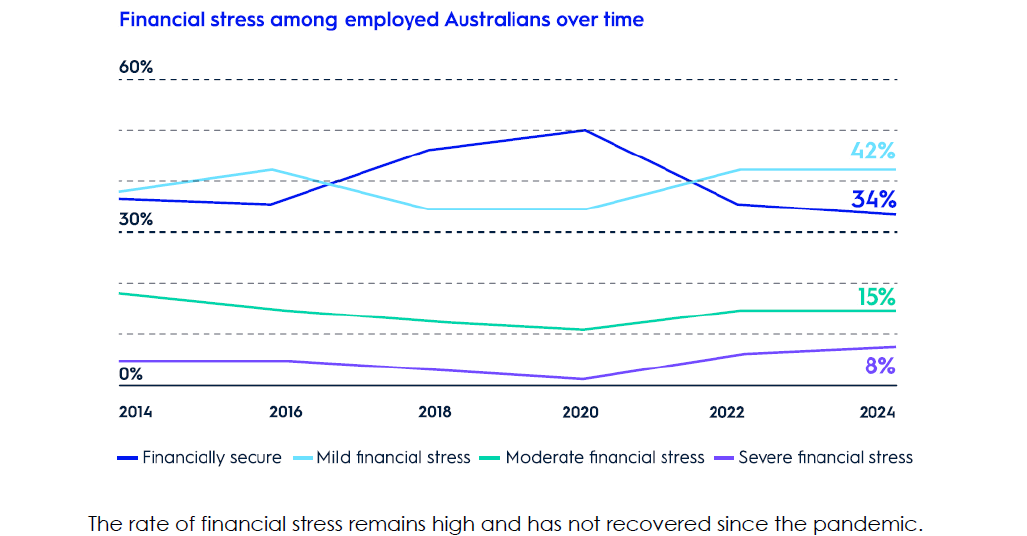

AMP’s Financial Wellness report, which surveyed 2,475 Australians aged 18 and over in July2 2024, found financial stress levels in Australia are now at their highest point in 10 years, with just one in three currently feeling financially secure.

Nguyen (pictured above), who services primarily PAYG wage earning clients and SME business owners living in Western Sydney, said he had noticed evidence of stress as interest rates rose.

“We did receive a lot more calls as the interest rates started going up and people were in a panic and whatnot, working out what they can do and what their options were, that sort of stuff,” Nguyen said. “So [financial] stress from that point of view was apparent.”

However, he said what he had noticed more than anything was that his clients, and Australians in general, were pretty resilient, and that in contrast to “doomsday scenarios” most had just been spending less.

“They did exactly what the RBA intended. They spent less as a whole.”

Nguyen said that, as many of his clients were good savers, they were also able to tap into savings. While these had been depleted, it had allowed them to weather the interest rate hikes.

“Everyone just rallied around the home, they wanted to protect their home, and they just spent less elsewhere.”

Australians are responding to the tough financial environment by spending less – the report found one in three Australians had cancelled streaming subscriptions and gym memberships.

AMP Bank group executive Sean O’Malley (pictured below) said the financial insecurity uncovered by the report was not surprising given cost of living pressures and housing unaffordability challenges being faced.

“And while the research tells us that most are meeting their mortgage repayments, we know that savings rates are down and many are cutting back expenditure on household basics such as groceries, and other more discretionary items such as streaming services and holidays,” O’Malley said.

Source: AMP Financial Wellness Index, July 2024

When it came to home loans, borrowers had focused on meeting their repayments.

“It’s an adage, isn’t it, that it always seems hard until you do it,” Nguyen said.

“There was a bit of panic, when people were saying, ‘How can I afford it?’. Well, guess what? They did afford it. When it comes to their home, you don’t sell your home just because the rates go up, you are thinking of other ways to keep your home.”

AMP found stress levels were also rising for those earning between $100,000 and $500,000, with one in four in this income bracket either ‘severely’ or ‘moderately’ financially stressed.

Nguyen suggested some of these borrowers may have been seduced by “lifestyle inflation”.

“Managing money is an art form. Some people have it. Some people don’t. Just because you have more of the income doesn’t mean you’re a better money manager,” he said.

Role for brokers to educate clients

AMP found many people were focusing on short-term financial demands rather than long-term planning, with one in three Australians saying they never or rarely planned for their financial future.

One in three Australians are also still not using any information sources at all to inform important financial decisions, even easily accessible information such as podcasts, social media, or Google.

This could provide an opportunity for finance brokers to support client education, though Nguyen said that his approach to client service was always the same, whether rates were going up or down.

“You always need to be in a position where you engage with us and we can help review your rates on a regular basis. Because we do that, the message has always been the same,” he said.

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!