We’re currently in a strange sort of housing crisis where existing homeowners are in a fantastic spot, but prospective buyers are mostly priced out.

The issue is both an affordability problem and a lack of available inventory problem. Namely, the type of inventory first-time home buyers are looking for.

So you’ve got a market of haves and have nots, and a very wide gap between the two.

At the same time, you’ve got millions and millions of locked-in homeowners, with mortgages so cheap they’ll never refinance or sell.

This exacerbates the inventory problem, but also makes it difficult for mortgage lenders to stay afloat due to plummeting application volume.

The solution? Offer your existing customers a second mortgage that doesn’t disturb the first.

Loan Servicers Want to Do More Than Service Your Loan

Over the past several years, mortgage loan servicers have been embracing technology and making big investments to ramp up their recapture game.

They’re no longer satisfied with simply collecting monthly principal and interest payments, or managing your escrow account.

Realizing they’ve got a goldmine of data at their fingertips, including contact information, they’re making big moves to capture more business from their existing clientele.

Why go out and look for more prospects when you’ve got millions in your own database? Especially when you know everything about your existing customers?

Everyone knows mortgage rate lock-in has effectively crushed rate and term refinance demand.

And cash out refinances are also a non-starter for many homeowners unless they have other really high-rate debt that’s pressing enough to give up their low-rate mortgage.

So lenders are left with a pretty small pool of in-the-money borrowers to approach. Still, thanks to their investments, they’re getting better and better at retaining this business.

Instead of their customers going to an outside lender, they’re able to sell them on a streamline refinance or other option and keep them in-house.

But they know the volume on first mortgages just isn’t there, so what’s the move? Well, offer them a second mortgage, of course.

Your Loan Servicer Wants You to Take Out a Second Mortgage

I’ve talked about loan servicer recapture before, where new loans like refis stay with the company that serviced the loan.

So if you have a home loan serviced by Chase, a loan officer from Chase might call you and try to sell you on a cash out refi or another option.

I’ve warned people to watch out for inferior refinance offers from the original lender. And to reach out to other lenders when they reach out to you.

But that was just the tip of the iceberg. You’re going to see a big push by servicers to get their existing customers to take out second mortgages.

This is especially true on conventional loans backed by Fannie Mae and Freddie Mac, for which borrowers are mostly locked-in and streamline options don’t exist.

They know you’re not touching your first mortgage, but they still want to increase production.

So you’ll be pitched a new HELOC or home equity loan to accompany your low-rate first mortgage.

As a result, you’ll have a higher outstanding balance and blended rate between your two loans and become a more profitable customer.

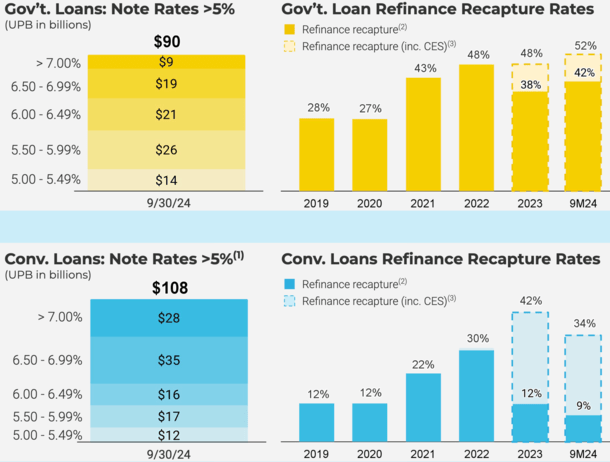

This is Pennymac’s approach, as seen above, which launched of closed-end second (CES) mortgage product in 2022. They are one of the nation’s largest mortgage servicers.

It allows their existing customers to access their home equity while retaining their low-rate, first mortgage. And most importantly, it keeps the customer with Pennymac.

Notice how much higher the recapture percentage is once they tack on a CES.

Other servicers are doing the same thing. Just last month, UWM launched KEEP, which recaptures past clients for its mortgage broker partners.

And let’s not forget Freddie Mac’s second mortgage pilot program, where they’ll begin buying the subordinate loans to improve market liquidity.

Second Mortgage Push Might Allow the Spending to Continue

One major difference between this housing cycle and the early 2000s one is how little equity has been tapped.

In the early 2000s, it was all about 100% cash out refis and piggyback seconds that went to 100% CLTV.

Lenders basically threw any semblance of quality underwriting out the door and approved anyone and everyone for a mortgage.

And they allowed homeowners to borrow every last dollar, often with faulty appraisals that overstated home values.

We all know how that turned out. Fortunately, things actually are a lot different today, for now.

If this second mortgage push materializes, as I believe it will, consumer spending will continue, even if economic conditions take a turn for the worse.

Lots of Americans have already burned through excess savings squirreled away during the easy-money days of the pandemic.

And you’re hearing about folks being a lot more stretched, not even able to weather three months without income. But if they’re able to access a new lifeline, the spending can go on.

Then you start to envision a situation similar to the early 2000s where homeowners are using their properties as ATMs again.

In the end, we might start to see CLTVs creep higher and higher, especially if home prices flatten or even fall in certain overheated metros.

The good news is we still have the highest home equity levels on record, and home equity lending remains quite subdued compared to that time period.

But it should be noted that it hit its highest point since 2008 in the first half of 2024. And if it increases substantially from there, we could have a situation where homeowners are overextended again.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.